Use our payment plan agreement to set up an installment plan between a lender and a borrower.

Updated March 26, 2024

Written by Sara Hostelley | Reviewed by Brooke Davis

A payment plan agreement is a legal contract that outlines how a debtor will pay back the creditor. A creditor can set up a payment plan agreement to make the debtor’s repayments more manageable, improving their chances of receiving the total debt amount back.

A payment plan is a way for someone to spread out the total amount owed into smaller, more manageable payments. The plan describes the terms to which both parties agree. It’s useful for borrowers who don’t want to or can’t pay the total amount for goods or services in a single installment.

Some common uses for payment plans include:

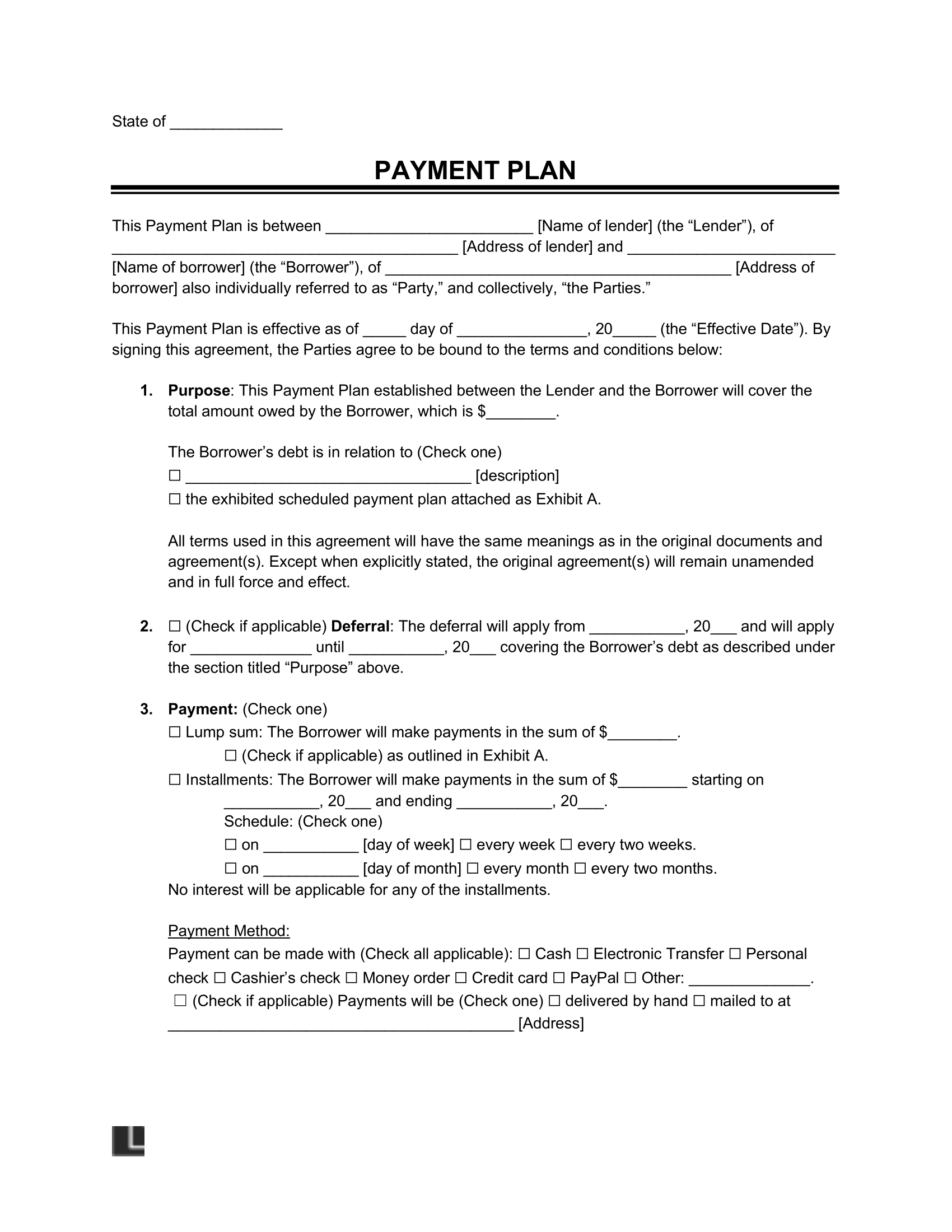

Parties’ Information: Identify the names and addresses of the creditor and debtor. Including this information can ensure both parties are easily identifiable.

Debt Acknowledgment: This clause acknowledges a debt the debtor owes to the creditor. It outlines the specific debt amount, the reason for the debt, and other details relating to the obligation.

Payment Schedule: Include the agreement’s start and end dates. Specify the timing and amounts of payments the debtor will make to the creditor.

Payment Methods: When writing a payment agreement, you should consider the payment method and the payment frequency. Clarify if the borrower will pay the full amount as a lump sum or pay in installments.

If the parties agree to regular payments, you must decide how often the payment frequency and amounts. You will also have to agree on what payment method the debtor will use.

Late Payments: Specify the penalties or consequences if the borrower fails to adhere to the repayment schedule. Detail late fees, interest charges, and other penalties for overdue payments.

Default Clause: Outline the conditions that signal a default on the debtor’s part. Explain the specific events or actions that initiate a breach of the agreement and the legal consequences that will follow.

Signatures: Your payment plan agreement won’t be legally binding without written consent from both the borrower and the lender. Signing the contract acts as legal proof that the involved parties have accepted the terms of the agreement.

Interest Rate: The interest rate clause explains the rate at which interest accrues on unpaid balances. It explains how the interest is calculated, compounded, and applied to the outstanding amount over the payment plan’s duration.

Discounted Balance: You may create an incentive for lump-sum or early payments by offering a reduced payoff amount or a discount on the total amount owed. It encourages the debtor to make prompt payments and ensures you receive your money back.

Prepayment Clause: The prepayment clause specifies if the payer can pay off the debt before the agreed-upon due dates without incurring additional penalties or fees. It clarifies the restrictions or conditions on prepayment and how early the debtor can make early payments.

Dispute Resolution: The dispute resolution clause explains procedures for managing disputes or disagreements arising from the payment plan agreement. It may explain methods such as arbitration or mediation.

Co-Signers (Guarantors): You may have the debtor add a co-signer or guarantor as a third party who agrees to accept responsibility for the debt if the original debtor defaults. This clause can be helpful when the debtor has a poor credit history, as it provides extra security to the creditor.

Meet with the borrower to determine payment plan options. Some borrowers may want to pay off the debt as quickly as possible in fewer payments, while others may wish to extend the payment period.

Review all sections and clauses with the borrower. Ensure they understand and agree to the entire agreement. Finalize the arrangement and convert it to a legally binding document by signing it as the creditor and obtaining the borrower’s signature.

Once the payment plan agreement is initiated, you can receive payments via the designated payment method. You may need to provide payment instructions, especially if you accept automatic payments via an online portal or credit card.

When the borrower meets all their payments on time and successfully reaches the end of the established period, you can release them as a debtor.

If the borrower falls behind on their expected payments, you can follow the payment plan agreement’s guidelines for defaulted payments.

Download our free payment agreement template in PDF or Word format below:

Create Your Payment Agreement in Minutes!